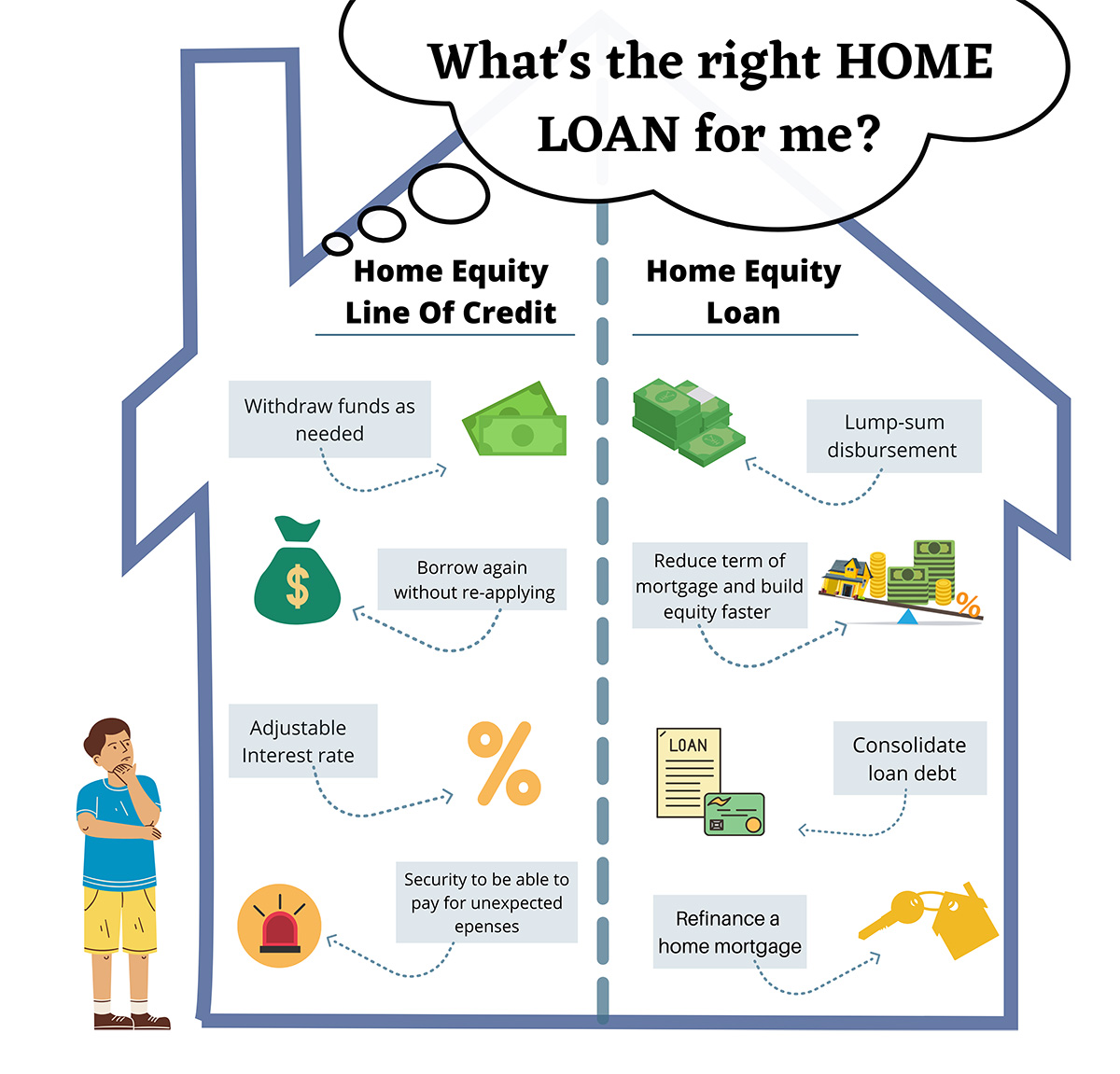

Equity Loan Options: Choosing the Right One for You

Equity Loan Options: Choosing the Right One for You

Blog Article

Debunking the Certification Process for an Equity Funding Authorization

Browsing the certification process for an equity funding authorization can often appear like figuring out a complex challenge, with various variables at play that figure out one's qualification. Recognizing the interaction in between debt-to-income ratios, loan-to-value proportions, and various other vital criteria is extremely important in securing approval for an equity finance.

Key Qualification Standard

To receive an equity lending approval, meeting details crucial eligibility standards is essential. Lenders normally require applicants to have a minimum credit report rating, frequently in the array of 620 to 700, depending upon the organization. A solid credit rating, showing a liable payment performance history, is also important. In addition, lenders examine the applicant's debt-to-income proportion, with the majority of liking a ratio below 43%. This demonstrates the debtor's capability to manage extra financial obligation responsibly.

In addition, lending institutions examine the loan-to-value ratio, which contrasts the amount of the financing to the evaluated value of the building. Usually, lending institutions choose a lower proportion, such as 80% or much less, to mitigate their threat. Work and earnings stability are crucial consider the authorization process, with lending institutions seeking guarantee that the debtor has a reputable resource of earnings to pay back the lending. Satisfying these key eligibility requirements boosts the likelihood of securing authorization for an equity funding.

Credit Rating Relevance

Credit report normally vary from 300 to 850, with higher scores being more positive. Lenders typically have minimum credit report requirements for equity lendings, with scores over 700 normally considered excellent. It's crucial for applicants to review their credit scores reports consistently, checking for any kind of errors that could adversely influence their scores. By preserving a great credit report with prompt expense payments, low credit scores utilization, and liable borrowing, candidates can enhance their opportunities of equity car loan authorization at affordable rates. Recognizing the importance of credit rating and taking actions to boost them can dramatically affect a borrower's economic opportunities.

:max_bytes(150000):strip_icc()/homeequityloan-e11896bf4ac1475a9806a55f92e0c312.jpg)

Debt-to-Income Ratio Evaluation

Offered the crucial role of credit rating ratings in identifying equity finance approval, an additional important aspect that lending institutions assess is a candidate's debt-to-income ratio evaluation. The debt-to-income proportion is an essential financial statistics that gives insight right into a person's capability to take care of extra financial debt properly. Lenders determine this proportion by separating the overall month-to-month debt obligations of an applicant by their gross monthly income. A lower debt-to-income proportion shows that a consumer has even more revenue offered to cover their debt settlements, making them a more appealing prospect for an equity funding.

Borrowers with a higher debt-to-income ratio may deal with difficulties in securing approval for an equity finance, as it recommends a greater danger of skipping on the car more tips here loan. It is vital for applicants to assess and potentially minimize their debt-to-income proportion prior to applying for an equity lending to enhance their opportunities of authorization.

Home Appraisal Demands

Assessing the worth of the home through a thorough appraisal is an essential action in the equity finance authorization process. Lenders need a residential or commercial property evaluation to make sure that the home offers adequate security for the lending amount asked for by the debtor. During the residential or commercial property appraisal, a certified appraiser assesses various aspects such as the residential property's problem, size, location, equivalent home worths in the location, and any kind of special functions that may influence its overall worth.

The residential or commercial property's assessment worth plays a critical duty in identifying the maximum amount of equity that can be borrowed against the home. Lenders generally need that the appraised value fulfills or exceeds a certain percentage of the funding amount, called the loan-to-value proportion. This ratio assists minimize the lending institution's danger by ensuring that the residential or commercial property holds adequate value to cover the loan in case of default.

Inevitably, a detailed property assessment is essential for both the lender and the consumer to accurately assess the residential or commercial property's worth and determine the feasibility of approving an equity car loan. - Equity Loan

Understanding Loan-to-Value Ratio

The loan-to-value ratio is a vital financial metric made use of by lending institutions to analyze the threat connected with providing an equity lending based upon the property's appraised value. This ratio is determined by separating the quantity of the finance by the evaluated value of the home. For example, if a home is evaluated at $200,000 and the lending quantity is $150,000, the loan-to-value ratio would be 75% ($ 150,000/$ 200,000)

Lenders make use of the loan-to-value ratio to determine the degree of threat they are taking on by giving a car loan. A greater loan-to-value proportion suggests a higher risk for the lender, as the borrower has less equity in the building. Lenders commonly like reduced loan-to-value ratios, as they give a padding in instance the consumer defaults on the finance and the building needs to be marketed to recuperate the funds.

Borrowers can additionally take advantage of a lower loan-to-value proportion, as it might lead to much better lending terms, such as reduced rate of interest or reduced charges (Alpine Credits Canada). Comprehending the loan-to-value proportion is critical for both loan providers and customers in the equity finance authorization process

Conclusion

Finally, the certification procedure for an equity lending authorization is based on vital eligibility requirements, credit report rating value, debt-to-income proportion evaluation, residential property evaluation needs, and recognizing loan-to-value proportion. Fulfilling these standards is essential for securing approval for an equity loan. It is crucial for debtors to meticulously evaluate their monetary standing and residential property value to boost their opportunities of approval. Understanding these aspects can help individuals navigate the equity lending approval procedure a lot more successfully.

Comprehending the interaction between debt-to-income proportions, loan-to-value ratios, and various other crucial standards is vital in safeguarding approval for an equity financing.Offered the essential function of debt scores in figuring out equity loan authorization, an additional essential element that loan providers analyze is a candidate's debt-to-income ratio analysis - Alpine Credits Home Equity Loans. Borrowers with a greater debt-to-income proportion may deal with challenges in protecting authorization for an equity car loan, as it suggests a greater threat of skipping on the lending. It is essential for applicants to analyze and potentially reduce their debt-to-income proportion prior to using for an equity car loan to raise their chances of approval

In conclusion, the certification procedure for an equity funding authorization is based on key qualification standards, credit report score value, debt-to-income ratio evaluation, home assessment demands, and recognizing loan-to-value proportion.

Report this page